Health Insurance for Expats in Germany

Understand public and private health insurance in Germany and learn how to choose the right structure for your income, family plans and long-term financial goals.

Health Insurance for Expats in Germany

Understand public and private health insurance in Germany and learn how to choose the right structure for your income, family plans and long-term financial goals.

Key Facts

Eligibility Matters

Only employees earning more than €77,400 gross annually (2026 threshold), self-employed professionals, civil servants, and students over 30 can switch from public health insurance (GKV) to private health insurance (PKV).

Public Insurance Is Income-Based

Public health insurance contributions are calculated as a percentage of your salary. Most employees pay around 14.6% plus an additional insurer-specific contribution, shared with the employer, up to the legal income cap.

Private Insurance Offers More Flexibility

Private health insurance allows you to customize coverage based on your needs, including specialist access, private hospital treatment, international coverage and additional medical services.

The Decision Is About More Than Monthly Costs

Public health insurance offers standardized coverage regulated by law, while private health insurance is a long-term financial and healthcare planning decision that should align with your income, family plans and future goals.

Understanding Health Insurance in Germany

Germany operates with two parallel healthcare systems: Public Health Insurance (GKV) and Private Health Insurance (PKV).

Both provide high-quality healthcare access, but they are built on fundamentally different financial structures.

Public insurance is based on collective cost sharing and income-linked contributions, while private insurance operates through individualized contracts and risk-based pricing.

The right system depends on factors such as:

- income

- employment structure

- family situation

- long-term residency plans

- financial goals

For expats, understanding these structural differences early is essential for avoiding costly long-term mistakes.

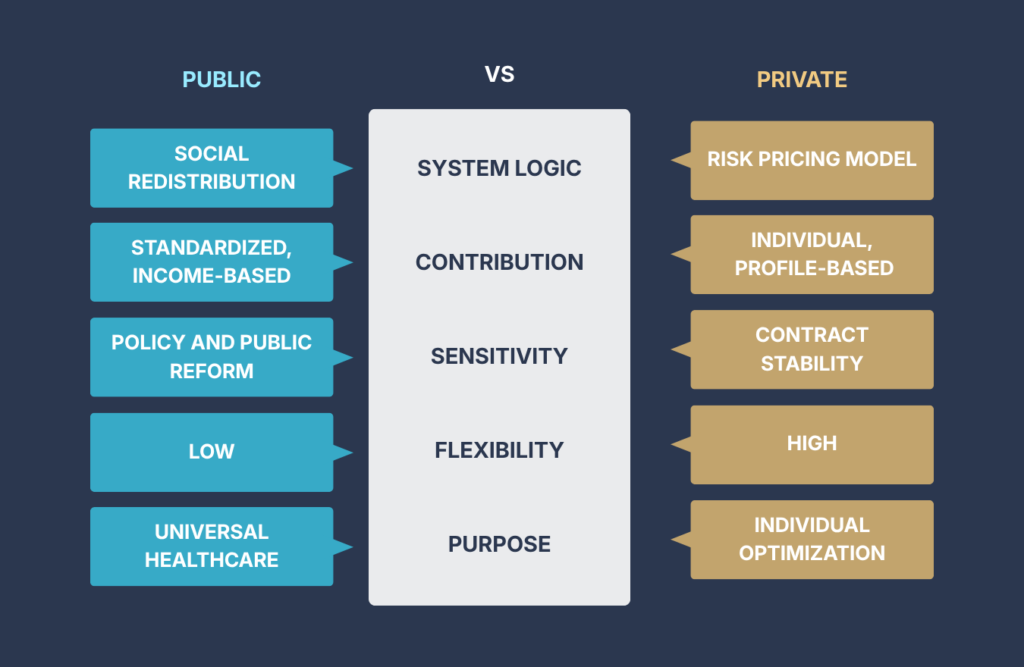

Structural Comparison

Public Health Insurance (GKV)

Stability Through Collective Risk Sharing

Public health insurance in Germany, known as GKV (Gesetzliche Krankenversicherung), is based on a solidarity model where contributions depend primarily on income rather than individual health risk.

This system is designed to guarantee broad access to healthcare while distributing costs collectively across society. For many expats, GKV offers stability, predictable administration and strong baseline healthcare coverage from the moment they arrive in Germany.

Unlike private health insurance, acceptance is generally not dependent on medical history or pre-existing conditions.

How GKV Works

Public health insurance contributions are linked to salary and automatically deducted through payroll.

The system is designed around:

- income-based contributions

- standardized healthcare coverage

- collective cost sharing

- regulated access to medical care

For employees, contributions are shared between employer and employee up to the legal contribution ceiling.

One of the largest advantages of GKV is family insurance. Non-working spouses and children can often remain insured without additional monthly contributions.

What Expats Should Know About GKV

GKV is often the safest and most straightforward solution for families with children, individuals with chronic health conditions, lower or mid-income earners, and expats seeking long-term predictability.

At the same time, the system is less flexible than private insurance. Coverage is largely standardized by law, meaning customization options remain limited compared to PKV.

Contribution levels may also increase over time as income rises or healthcare costs change politically and economically.

The Long-Term Perspective

Public health insurance is not designed to maximize individual optimization. Its purpose is stability, accessibility and broad social protection.

For many expats, this creates exactly what they need:

- reliable healthcare access

- financial predictability

- strong family protection

- peace of mind during long-term residency in Germany

Private Health Insurance (PKV)

Personalized Healthcare and Long-Term Financial Structuring

Private health insurance in Germany, known as PKV (Private Krankenversicherung), operates under a completely different model from public insurance.

Instead of collective redistribution, PKV uses:

- individual risk assessment

- contract-based coverage

- actuarial pricing structures

This creates a system where healthcare is structured around the individual rather than the broader population.

How PKV Works

Private health insurance pricing depends primarily on age at entry, health status, selected coverage level, and long-term tariff structure.

Unlike GKV, contributions are not directly linked to income. This means high earners may benefit from significantly different long-term cost structures depending on their personal situation.

Coverage can also be tailored more precisely, including:

- specialist access

- private hospital treatment

- international coverage

- enhanced dental and vision benefits

- alternative medicine options

Why Many Expats Consider PKV

For eligible expats, PKV may offer greater flexibility, faster access to appointments, personalized coverage structures, and independent scaling of contributions tied to salary growth.

In many cases, PKV is not only a healthcare decision but also part of a broader financial planning strategy.

Health insurance contributions may partially reduce taxable income through deductible basic coverage components, which can improve long-term tax efficiency for higher earners.

Important Long-Term Considerations

Private health insurance requires significantly more long-term planning than GKV.

Important factors include:

- future income development

- retirement affordability

- family planning

- long-term residency intentions

- premium development over time

PKV is often misunderstood as simply “better” or “worse” than public insurance. In reality, it is a parallel system designed around different economic principles. The right structure depends entirely on the individual situation.

Example Cost Comparison

Monthly contributions between public and private health insurance can differ significantly depending on income, age, family structure, and chosen coverage.

The example on the right illustrates a simplified comparison for a 30-year-old employee earning €80,000 gross annually.

The right health insurance strategy is not only about today’s costs. Changes in income, family circumstances, regulations, and insurance tariffs can significantly affect the long-term efficiency of your setup.

Whether you are publicly or privately insured, periodic reviews help ensure your coverage remains aligned with your financial goals and life plans.

Note: Actual costs depend on: insurer, tariff structure, health profile, deductible level, family situation, and long-term planning strategy.

Example Cost Comparison

Monthly contributions between public and private health insurance can differ significantly depending on income, age, family structure, and chosen coverage.

The example below illustrates a simplified comparison for a 30-year-old employee earning €80,000 gross annually.

The right health insurance strategy is not only about today’s costs. Changes in income, family circumstances, regulations, and insurance tariffs can significantly affect the long-term efficiency of your setup.

Whether you are publicly or privately insured, periodic reviews help ensure your coverage remains aligned with your financial goals and life plans.

Note: Actual costs depend on: insurer, tariff structure, health profile, deductible level, family situation, and long-term planning strategy.

Which System Fits Which Scenario?

Which Health Insurance System Fits Your Situation?

There is no universally “better” system in Germany. The right choice depends on your personal, financial and long-term circumstances.

GKV may be more suitable if you:

- have children or a non-working spouse

- prefer predictable administration

- value collective protection structures

- expect fluctuating income

- have existing health conditions

- want maximum simplicity and stability

PKV may be more suitable if you:

- earn above the mandatory insurance threshold

- are self-employed or a high-income employee

- want more individualized healthcare access

- value coverage customization

- plan long-term financial optimization

- are comfortable making strategic long-term decisions

The Most Important Factor

The decision between GKV and PKV should not be based only on short-term monthly costs. The more important considerations are:

- long-term affordability

- family planning

- tax structure

- retirement planning

- income trajectory

- future residency plans

For many expats, the biggest mistake is not choosing the “wrong” system, but remaining in a structure that was never optimized for their situation in the first place.

Long-Term Planning

Health Insurance Is Also a Financial Planning Decision

Health insurance in Germany affects much more than medical access. The chosen system directly interacts with:

- taxable income

- retirement planning

- wealth accumulation

- family protection

- long-term monthly obligations

- financial flexibility

For high-income expats in particular, health insurance becomes part of a broader financial structure rather than a standalone product. This is especially important in Germany, where healthcare, taxation, and retirement systems are closely interconnected.

A well-structured decision today can influence long-term financial stability for decades.

FAQ

Frequently Asked Questions

Can I switch from GKV to PKV at any time?

No. Employees generally need to earn above the annual mandatory insurance threshold to become eligible for private insurance. Self-employed individuals and certain other groups may qualify under different rules.

Is private health insurance always cheaper?

Not necessarily. Costs depend heavily on age, health profile, coverage structure and family situation. In some cases PKV may initially cost less, while in others GKV may remain financially more efficient long-term.

Can I return from PKV to GKV later?

Returning to public insurance can become difficult depending on age, employment structure and residency situation. This is one reason why long-term planning is extremely important before switching systems.

Does GKV cover family members?

Yes. Non-working spouses and children are often covered under public insurance without additional monthly contributions.

Does PKV offer better healthcare?

Both systems provide high-quality healthcare in Germany. The difference lies more in structure, flexibility, access and customization rather than basic medical competence.

Is health insurance tax deductible in Germany?

Parts of both GKV and PKV contributions may be tax deductible, particularly the basic healthcare coverage components.

Which option is better for expats?

There is no universal answer. The right structure depends on income, family plans, long-term residency intentions and financial goals.

Unsure Which Health Insurance Structure Fits Your Situation?

Health insurance decisions in Germany can affect your long-term financial structure, taxes and healthcare access for decades. We help expats evaluate:

GKV vs PKV suitability

long-term contribution development

family scenarios

tax efficiency

retirement affordability

overall financial alignment

Unsure Which Health Insurance Structure Fits Your Situation?

Health insurance decisions in Germany can affect your long-term financial structure, taxes and healthcare access for decades. We help expats evaluate:

GKV vs PKV suitability

long-term contribution development

family scenarios

tax efficiency

retirement affordability

overall financial alignment